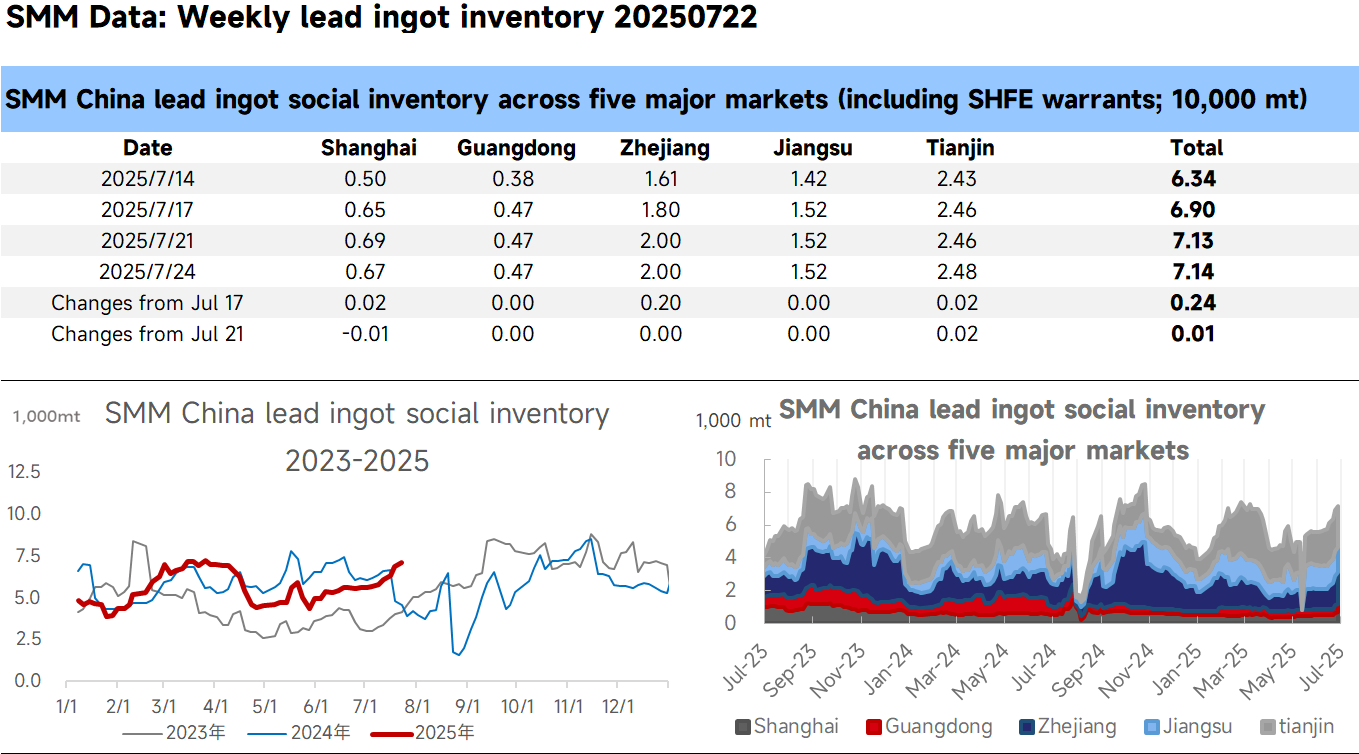

The impact of maintenance at some primary lead enterprises this week has not yet been fully lifted. Meanwhile, the losses in secondary lead production have not improved, and secondary lead smelters have low production enthusiasm. During this period, smelters mostly refused to budge on prices when shipping goods. Secondary refined lead was quoted at premiums of 0-100 yuan/mt against the SMM #1 lead average price, while primary lead (electrolytic lead) in major producing regions was quoted at discounts of 20 yuan/mt to premiums of 50 yuan/mt against the SMM #1 lead price. The price advantage of secondary lead has declined, causing downstream enterprises' rigid demand to flow towards primary lead. Correspondingly, the quotations for cargoes in social warehouses were relatively firm, with prices in the Jiangsu, Zhejiang, Shanghai region quoted at discounts of 50-30 yuan/mt against the SHFE lead 2508 contract or discounts of 20-0 yuan/mt against the SHFE lead 2509 contract. In comparison, downstream enterprises' rigid demand was more inclined towards purchasing cargoes self-picked up from production sites at smelters. As a result, the in-plant inventory at smelters in major producing regions declined this week, while social warehouse inventory still saw a slight increase.